Emerging Champions: Small-Cap Stocks with Hidden High-Growth Segments (And 7 Worth Watching)

How investors can generate returns by analyzing the overlooked business segments hidden inside seemingly ordinary companies

In the mid-1950s, workers at a modest Bangkok temple made a startling discovery. While moving an old Buddha statue, the ropes suddenly snapped. The figure crashed to the ground, cracking its dull stucco exterior. What peeked through stunned everyone: a simmer of gold. As monks carefully chipped away the outer layer, they uncovered what had been hidden for centuries—the world’s largest solid-gold Buddha, weighing over five tonnes.

Fascinating story.

And also a good starting point for today’s article.

In markets, you can often find these “golden Buddhas”; companies that, at first glance, seem plain and unremarkable. But when you dig into the filings or listen closely to management calls, you may uncover something just beneath the surface: a high-growth, high-margin business segment emerging within the company.

It’s not obvious in the consolidated numbers. But it’s there.

That’s what this piece is about: emerging champions.

Why the Market Misses These Companies

How can the market miss a fast-growing, wildly profitable business segment? Well, there could be several reasons.

For one, there's a scale bias baked into how institutional money thinks. If a new software division makes up 15% of sales at a tiny industrial firm, it’s just noise to most analysts; it doesn’t “move the needle.” That bias leads many to skip over it entirely, even if it’s growing like wildfire.

Another reason? Coverage is thin to nonexistent. The majority of these companies are flying under the radar, and without consistent coverage, even a booming segment can go completely unnoticed.

Then there’s the way these businesses report. If you’re just skimming top-line revenue or net income, you’ll likely miss the real story. Many of these firms lump their most promising ventures into generic categories like “Other” or “Corporate.” Unless you’re willing to go through footnotes, MD&As, or cross-check earnings call remarks, you’ll never see the breakout taking shape.

There’s also a psychological trap at play, I’ve read that some behavioural psychologists call inattentional blindness. When investors come in with a story already in mind, say, “this is a boring no-growth manufacturer” they ignore anything that doesn’t fit. Even if a tech-enabled subscription business is emerging inside the company, it gets ignored because the narrative has already been set.

Finally, legacy drag is another big reason I’ve seen these stories stay hidden. When the businesses is in transition (the old and troubled line is fading, but something new is gaining steam), the market tends to fixate on the decline and fail to re-rate for the growth at least for a while. Yesterday’s problems overshadowing tomorrow’s potential.

Put it all together—coverage gaps, mental shortcuts, messy disclosures, and legacy bias—and you’ve got the perfect storm for a disconnect between perception and reality. Because what looks like a boring small-cap might actually be what I like to call a coiled spring.

How to Spot ’Em: Follow the Breadcrumbs

So how do I actually go about finding these “emerging champions” before the broader market catches on? Let’s take a look.

The first place I look is segment reporting. Big divergence between segment metrics usually means something interesting is happening under the hood.

Next, I read management commentary. Shareholder letters, earnings calls, MD&As; these are full of breadcrumbs.

Then I follow the money (and the people). Capital allocation tells you what management really believes in. If I see most of the capex, M&A spend, or hiring efforts going into one part of the business, it’s usually a sign that’s where they see growth. Expanding headcount, new facilities, niche hires; these are all signals.

Finally, I look for signals from insiders or savvy outsiders. If executives or board members are buying shares while a new segment is ramping, that could be a sign that they see a lot of potential in that particular segment.

Yes, this kind of research takes more work. Or, of course, you could just throw all the 10-Ks into NotebookLM or ChatGPT and see what they find.

When Mr. Market Wakes Up: How Hidden Value Gets Unlocked

Finding an emerging stellar segment is step one. Step two is getting paid, which usually means waiting (and hoping) for that hidden engine to become recognized and properly valued.

So, how does that recognition typically happen?

Sometimes, the path could be as simple as organic growth. The segment just keeps compounding, quarter after quarter, until it’s too big to ignore.

Other times, it’s corporate action that unlocks the value. Maybe management decides to spin off the high-growth segment, or sells it outright to a strategic buyer.

Then there’s the more subtle stuff: carve-outs, strategic partnerships, or enhanced disclosure. When a company starts breaking out segment results more cleanly or lists a minority stake in a hot division, it can trigger a kind of price discovery moment.

Of course, not every thesis resolves quickly. I can take time. The segment keeps growing, the core thesis is holding, but the stock goes nowhere for quarters (years?). That’s where conviction and patience matter. If the growth is intact and the rest of the business isn’t falling apart, I’m usually happy to wait. I keep coming back to Graham’s quote: in the short run, the market is a voting machine; in the long run, it’s a weighing machine. Eventually, weight wins.

7 Companies Hiding High-Performing Business Segments

Alright, let’s look at some real-world examples of these kinds of situations. None of these are investment recommendations or full deep dives (there’s always more nuance to consider). Mind that the only criterion for inclusion here is simple: each company has a hidden, high-performing business segment that may be overlooking by the market.

Let’s dive in.

IDT Corporation (IDT)

Probably not a secret anymore; I think it’s already clear there’s a much more interesting story unfolding here. Beneath the surface, IDT is transforming into a fintech and B2B services platform.

The real drivers now are National Retail Solutions (NRS) and BOSS Money. Both are growing revenue at light speed year over year, and they’re pushing overall gross margins to record highs—37.1% last quarter. Fintech gross profit is up 31%, and that’s what’s really behind the EPS surge: $0.86 GAAP EPS in Q3 FY25 versus just $0.22 a year ago. Meanwhile, the old-school telecom business is fading into the background, with flat overall revenue hiding just how strong the new segments are.

High-growth fintech pieces could command much higher multiples if they were separated out. I believe management has a solid track record of creating value through spin-offs, and I think we could see them go that route again. That said, I’m keeping an eye on two things: whether the telecom side erodes faster than digital grows, and whether they actually execute on a fintech spin or sale.

Below the numbers on their segment growth for NRS:

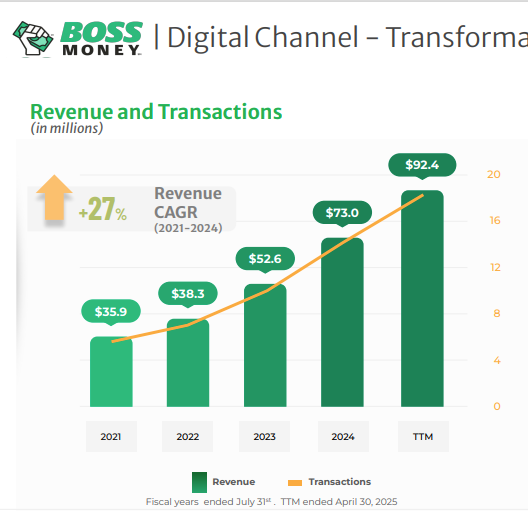

For Boss Money:

And for a third fast growth segment they have:

By the way, I’m thinking about doing a deep dive on this one. Shoot me a message if you find it interesting or have any insights—happy to connect.

Let’s keep going.

VSE Corporation (VSEC)

Technically, not a small-cap anymore. The real story here is their Aviation segment, which is definitely taking off. In Q4 alone, aviation revenue jumped 48% year over year with record-level profitability. Yet you wouldn’t know it from the consolidated EPS, which was down in 2024.

Why the disconnect? The legacy segments were dragging them down. The federal services business was already spun off, and they also sold the underperforming Fleet segment for $230 million in April.

If you strip the noise out, what you’re left with is a focused, high-growth aviation distributor whose core earnings power is expanding fast—up more than 40% last year. Just the Fleet sale alone accounts for a big chunk of the current market cap, which tells me the remaining Aviation business is being undervalued.

Of course, there are risks. They’ve made a few acquisitions and integration always comes with challenges. Plus, they’re still exposed to discretionary airline spending, which can swing with the cycle.

First Quarter 2025 Aviation Segment Results:

Kratos Defense & Security Solutions, Inc. (KTOS)

I’m always trying to look for companies with tailwind on their back. Kratos1 caught my eye for one reason: its Unmanned Systems segment. This is one of the few public companies offering real exposure to tactical drones and target UAVs.

Right now, Kratos is throwing cash into this opportunity which means consolidated profits are pretty much flat. The drone and space tech business is operating in a high-priority niche for the Pentagon.

That said, I’m aware of the risks. Defense contract timing is notoriously unpredictable, any delay or cancellation could hit hard. Plus, Kratos uses stock issuance to fund growth, which creates short-term dilution. Still, if you believe in the long-term demand for tactical drones, Kratos could be your emerging champion.

CSP Inc. (CSPI)

The standout here for me is their High-Performance Products (HPP) segment, anchored by ARIA cybersecurity and Myricom network solutions. It only made up about 8% of FY2024 revenue, but the margins? Nearly 65%. That’s a world apart from their low-margin legacy VAR business, which still accounts for 92% of sales.

HPP is starting to benefit from serious structural tailwinds in network security and defense. One of the recent wins (a multi-year ARIA contract) points to growing demand, and the new ARIA Zero Trust product could be a game changer. The problem is, you wouldn’t know any of that from the headline numbers. Overall FY2024 revenue fell 15%, mostly due to some one-time deals that didn’t repeat, and last year’s earnings were juiced by a tax credit.

Right now, the market sees CSPi as a stagnant tech reseller with flat topline and breakeven profits.

That said, I’m watching for traction on ARIA adoption. HPP is still small, and management needs to prove they can monetize it effectively. But if they can execute, CSPi could go from overlooked to revalued.

Babcock & Wilcox Enterprises, Inc. (BW)

When I broke down Babcock & Wilcox’s business, one segment jumped out immediately: Environmental. In 2024, revenue from that unit held steady around $109 million, but adjusted EBITDA more than doubled, up 161% to $10.8 million.

The problem is, consolidated results still look messy: $717 million in revenue, but a $73 million net loss. That’s mostly thanks to issues in the Renewable segment, where legacy projects are winding down, and ongoing burn from BrightLoop, their moonshot hydrogen tech. Add in high interest expense (there’s tons of debt), and the headline numbers obscure the real earnings power.

What keeps me interested is that both Environmental and the Thermal segment (boiler services and related power gen work) are actually performing well. Thermal, in particular, has a record backlog, and the company-wide backlog is up 47% year over year.

Mind that here, the risks are real: they’ve got heavy leverage, execution has to be tight, and any slip in environmental margins could set them back. But the stable businesses here are something to watch.

CECO Environmental Corp. (CECO)

CECO isn’t on many investors’ radars, but there’s probably something special happening beneath the surface, particularly in their Engineered Systems segment. This is where CECO delivers large-scale air pollution control and fluid handling solutions, and it’s become the backbone of the company’s growth story.

In Q4 2024, orders in this segment surged, pushing the backlog to a record $540.9 million—up 46% year over year. That’s demand driven by major trends like reshoring of industrial manufacturing, expanding data center infrastructure, and power generation upgrades.

CECO’s overall sales in 2024 only rose about 2%, and if you’re just scanning EPS or top-line growth, you might miss the shift happening underneath.

Risks? For sure. They’ve got to execute on that massive backlog; timing and cost control matter. And if macro conditions soften, some of those capex-heavy projects could get pushed out. But I like what I see here: a business pivoting hard toward higher-value markets with real momentum already showing up in the numbers.

BlackBerry Limited (BB)

Ok, I’ll end with BlackBerry. Yes, I know—it’s a controversial one. But lately, I’ve been seeing quite a few bullish write-ups on the name.

When I look into BlackBerry’s latest numbers, you can see that the IoT business is crushing it. In Q4, the QNX-powered IoT division hit a record $66 million in revenue, with gross margins around 83%. But you’d never know it from the company’s overall results, which are still weighed down by a floundering cybersecurity segment that’s barely growing.

Conclusion

All these examples show that emerging segments, or emerging champions, can appear in all kinds of companies, across industries and geographies. They’re out there. You just have to look beyond the headline numbers to find them.

In the end, spotting emerging champions means being willing to dig deeper and question the dominant narrative. So I try to keep my eyes open, stay curious and remember that the one who flips over more stones usually wins.

P.S. This is something I’ve been experimenting with (and with really good results!) If you like and restack this post to help boost its visibility, I’ll send you a PDF with three more companies I’m tracking that fit the “emerging champion” profile: hidden high-growth segments the market hasn’t priced in yet. Think of it as a bonus watchlist for those who want to go deeper.

Disclaimer

This newsletter (the “Publication”) is provided solely for informational and educational purposes and does not constitute an offer, solicitation, or recommendation to buy, sell, or hold any security or other financial instrument, nor should it be interpreted as legal, tax, accounting, or investment advice. Readers should perform their own independent research and consult with qualified professionals before making any financial decisions. The information herein is derived from sources believed to be reliable but is not guaranteed to be accurate, complete, or current, and it may be subject to change without notice. Any forward-looking statements or projections are inherently uncertain and may differ materially from actual results due to various risks and uncertainties. Investing involves significant risk, including the potential loss of principal, and past performance is not indicative of future results. The author(s) may hold or acquire positions in the securities or instruments discussed and may buy or sell such positions at any time without notice. The views expressed are those of the author(s) and are subject to change without notice. Neither the author(s) nor the publisher, affiliates, directors, officers, employees, or agents shall be liable for any direct, indirect, incidental, consequential, or punitive damages arising from the use of, or reliance on, this Publication.

Another “not small-cap”.

Interesting list

I'm definitely interested in your take on IDT. I am quite bullish (https://open.substack.com/pub/compcap/p/idt-q3-2025-riding-the-wave?utm_source=share&utm_medium=android&r=l1sdn) and am thinking that if you capitalize parts of R&D and SGA as they invest through that kind of spending, you get high Owner Earnings estimates.

And the traditional telecoms segment appears to have slowed /stopped it's decline and improves cost efficiencies...

Have you looked at Thinkific (TSX: THNC)? It seems like this could fit your framework. Their Self-serve business, which targets smaller customers, has struggled to show meaningful growth. Meanwhile, their Plus offering, which targets larger enterprise customers, is growing 25-30% every quarter and becoming a bigger part of the pie.