Second-Order Effects of Tariffs: Navigating Investments in a Fragmented Global Economy

How to assess company mitigation plans for navigating current and future trade turbulence and tariff-proof your portfolio

In the last few months, during meetings or calls with CEOs, tariffs has been an unavoidable topic for discussion. More often than not, the conversation tends to center on whether their companies are selling to or sourcing from any of the nations caught up in this tariff tussle and that’s it. I can’t help wondering—is that all there is? Could there be other, less obvious risks tied to tariffs that might emerge further down the line? What about the competitive dynamics?

Putting pen to paper—or, in this case, fingers to keyboard—is a good way to start thinking about the implications. Let’s dive in!

Unpacking Tariff Exposure

I think that the key to understand the full risks posed by tariffs in any company is to peel back the layers of their operations. As a discerning investor, it’s worth starting with a few key indicators to figure out what’s really going on.

Supply Chain Dependencies: Where’s Everything Coming From?

Let’s talk about supply chains first.

The first step, of course, is mapping out where a company manufactures its products and sources its critical parts. If a firm depends heavily on just one country—or a small handful of them—for essential components, it’s walking a tightrope.

Just imagine a manufacturer sourcing 80% of its parts from, say, East Asia. If tariffs suddenly hit there, that’s an easy to detect vulnerability. But that’s not always the case. Sometimes the risk could be buried in the details—intermediate parts might crisscross borders multiple times before the final product comes together. Are the parts sourced by the manufacturer being tariffed in other countries before they reach actual sourcing country? If so, will this generate an unexpected increase in COGS?

The more tangled and global the supply chain, the more probable it is to get hit by tariffs at any part of the supply chain.

So, what should you look for?

Check how concentrated their suppliers are and whether they’re adopting “China+1” strategies—shifting some production to places like Vietnam, India, or Mexico. Companies that’ve already spread out their production should handle trade policy curveballs better.

Market Concentration: Where’s the Money Coming From?

The next logical step is to consider where a company’s sales are concentrated.

If their revenue hinges on one foreign market, trouble could brew if that market gets caught in a trade spat. Take U.S. firms generating big sales from China or Europe—they’re prime candidates for retaliation if the U.S. hikes its tariffs.

Flip the script, and a non-U.S. company reliant on American buyers might see its goods slapped with border taxes, that’s probably the most common case we all think about.

According to MSCI, about 18% of global corporate revenue is exposed to U.S. tariffs and counter-tariffs—split roughly evenly between non-U.S. firms selling into the U.S. and American companies exporting abroad.

The trick is knowing your revenue mix. I understand that tools like MSCI’s Economic Exposure data can break it down by geography, spotlighting any hidden trouble zones. If a company’s generating, say, more than 25% of its sales from a single foreign country, that’s a red flag waving for tariff risk.

Regulatory Vulnerability

Now, not everything revolves around dollars and cents—politics and regulations play a big role too.

Is the company’s industry a frequent target for trade regulators or lawmakers? Steel, aluminum, solar panels, and appliances have all taken hits in the past. Tech and telecom firms might face what I’d call “undercover tariffs” or “tariffs in disguise”—think export controls or sanctions.

A good place to start is their public filings, like the 10-K risk factors section, or even industry news. Have they pushed for tariff exemptions before, or been affected by anti-dumping duties? If a company’s banking on favorable trade deals or lax enforcement, a single policy shift could throw them off balance.

In short, I think building a checklist for every company in your portfolio is a good idea. How diversified is their supply chain? Where are their big markets? Is their industry a political hot potato?

By piecing together where they source their raw materials and where they sell them, you'll get a sharper view of their tariff exposure. Some companies might sound vulnerable but have solid mitigation plans; others might seem fine until you dig deeper. There's more nuance to this than it appears at first glance. Let's see why.

Safe Havens and Shaky Stocks

You can’t get the full story by focusing on just one angle—it takes a a macro and micro approach to have the better sense of the situation.

The Big Picture (Macro)

Even the U.S. Federal Reserve’s paying attention—Powell recently pointed to tariffs as a reason they bumped up their inflation forecasts, these moves ripple into things like prices, interest rates, currency swings, and GDP growth.

So, what should we keep an eye on? Things like trade policy indices, PMIs, exchange rates, and bond yields—they’re clues to how tariffs (or even just tariff talk) are shaping the landscape.

I’m no macro investor, but a big takeaway from 2018-2019 was that there was way more tariff chatter than action. Lesson learned: not jumping at every headline. Let's see what happens this time but I suspect that the harder the tariff talk gets, the more probable it is that they are short lasting.

The Granular View (Micro)

On a micro level—can they pass on higher costs if tariffs hit? If they’ve got pricing power, their margins might hold up (though watch for demand dropping off). If not, you might need to trim your profit expectations in a tariff scenario.

Balance sheets matter too—a company with cash in the bank can weather short-term hits, like stockpiling inventory or swallowing tariff costs, while a leveraged one might buckle if cash gets tight. At its core, the micro lens is about resilience.

Of course, some companies has been working on their supply chains since the first round of Trump’s tariffs on China.

Since 2018, U.S. imports from China dropped 21% to about 14% today, with firms rerouting to Mexico or Southeast Asia—a massive shift driven by tariff worries.

Companies that jumped on “friendshoring” or “reshoring” have cut their exposure.

There is strong evidence of companies rerouting supply chains to Mexico. I fact, Mexico surpassed China as the largest U.S. import partner in 2023. This shift has been driven not only by the Trump tariff’s continued by Biden but also by:

The COVID-19 pandemic disrupting Asian supply chains

The USMCA free trade agreement

What happens with Mexico and Canada's tariffs remains uncertain. One compelling hypothesis suggests Mexico might match US tariff levels on China, helping create a North American trading bloc against Chinese imports. This strategic move could shield Mexican exports from facing tariffs when entering the US market.

This scenario creates important implications for businesses' competitive positions. Consider your company's supply chain structure: Are you importing semi-finished Chinese components for final assembly in Mexico before exporting to the US? Or have you developed a fully Mexican-sourced supply chain? The temporary exemption until April 2, 2025, for products that meet specific USMCA rules of origin is a step in that direction.

These supply chain decisions could dramatically reshape market share across entire industry segments, potentially creating winners and losers based solely on sourcing strategy.

So far though, the evidence shows that Mexico is preparing retaliatory measures directly against the US in response to the 25% tariffs imposed by Trump on March 4, 2025. We’ll see what happens.

Now, which are the sectors or industry that are usually more at risk?

Sectors Under Fire

Tariffs tend to target specific sectors—sometimes for strategic reasons like defense or tech, sometimes for political leverage (think farm states), or simply because that’s where global trade flows thickest. As investors, it’s worth figuring out which industries might find themselves in the hot seat given today’s geopolitical climate. Below there’s a good summary of the situation:

Let’s break it down.

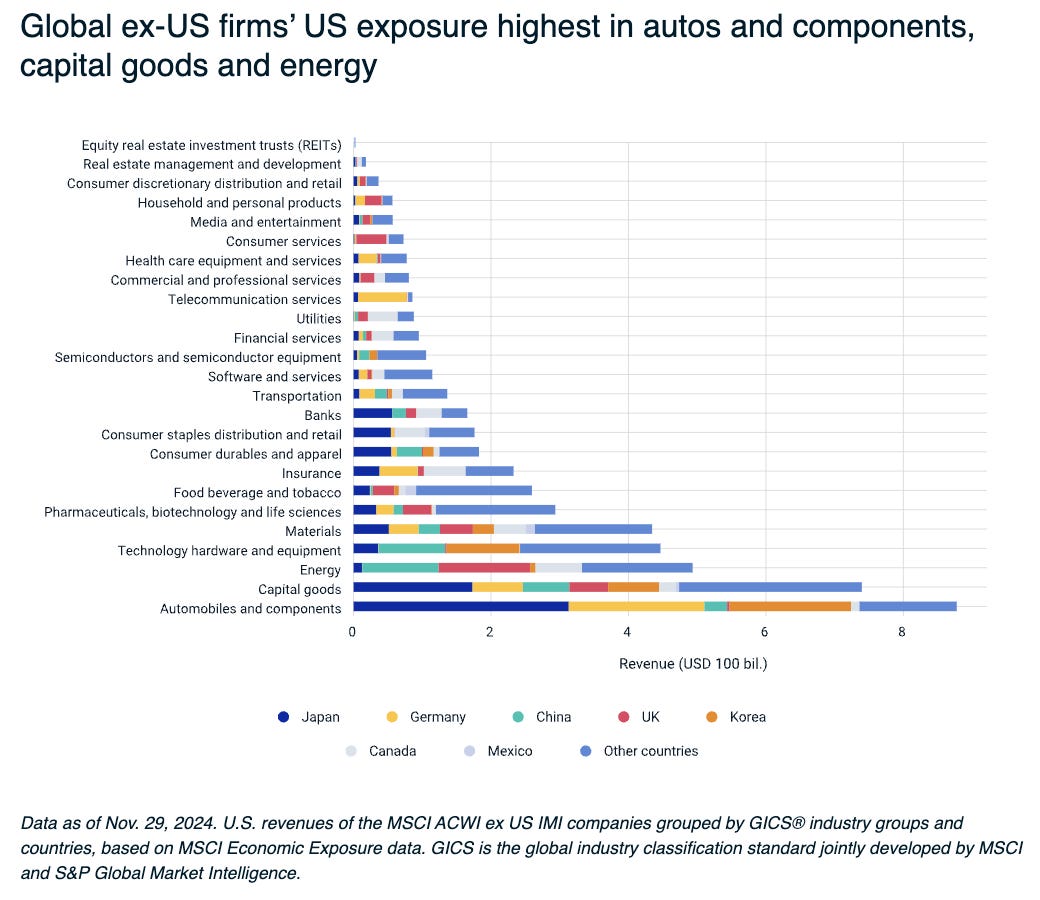

Automotive: The Car Industry’s Trade Woes

First up, the auto industry—it’s practically the poster child for trade disputes.

Cars and their parts zip across borders, especially in North America, Europe, and Asia. When trade tensions flare, this sector’s right in the spotlight.

Take Japanese and German brands building cars in Mexico, for instance. If the U.S. keeps the tariffs on Mexican imports, they’d feel the sting hard. Ford’s CEO, Jim Farley, didn’t mince words: broad auto tariffs could cost U.S. carmakers billions while handing a golden opportunity to foreign rivals who dodge the hit—like Korean or Japanese firms shipping from Asia.

I know Trump granted a temporary exemption for vehicles that meet specific USMCA (United States-Mexico-Canada Agreement) rules of origin requirements. This exemption began on March 7, 2025, and will remain in effect until April 2, 2025, but I think the coin is still in the air to see what happens.

In 2018, steel and aluminum tariffs increased costs, shaving about $1 billion off Ford’s profits, while foreign retaliation targeted U.S.-made cars, pushing companies like Harley-Davidson to move some production overseas.

Whether it’s raw materials or finished vehicles, autos get hit from all angles.

Below there’s an example of how integrated is the North American auto supply chain:

Technology Hardware & Semiconductors

Then there’s tech—specifically hardware and semiconductors—which has become a battleground for global power plays.

Back in the U.S.-China trade war, electronics like phones and laptops landed on tariff lists—though some rollouts were stalled to dodge consumer angst. Companies like Apple, Cisco, and Dell had to hustle, rerouting supply chains or ask for exemptions.

Looking at 2025, with U.S.-China tech tensions still simmering, this sector’s not out of the woods. We’re already seeing “stealth tariffs”—tighter export rules and chip bans that act like trade barriers without the label.

If you’re investing here, keep an eye on firms that’ve spread assembly beyond China with a “China+1” approach or stockpiled inventory as a buffer.

Energy and Commodities

Now, energy and commodities—oil, gas, metals—haven’t traditionally been tariff magnets. Energy security often trumps trade wars. But 2025 might be the year this changes.

Firms with cross-border pipelines or export routes—like LNG shippers or Canadian crude producers—could be affected on a permanent way.

Metals and mining aren’t safe either; 2018’s steel and aluminum tariffs hurt users like manufacturers while favouring some local producers.

Even green commodities are in play. The EU’s Carbon Border Adjustment Mechanism1—basically a tariff on carbon-intensive imports—will hit steel, aluminum, and cement exporters to Europe. Companies in lax-regulation regions might lose ground in Western markets.

History shows trade wars rarely focus on crude oil2 (OPEC+ drama aside), but oddballs like the 2018 solar panel tariffs3 disrupted renewables, so every option is on the table.

Agriculture & Food: The Political Pawn

Agriculture and food? They’re often front and center in trade wars—high-profile targets for retaliation.

Today, any country countering U.S. tariffs might zero in on American farms to hit politically sensitive spots. Soy, corn, meat, dairy—their demand can swing wildly with tariff moves.

On the flip side, nations exporting food to the U.S.—like Canadian beef or Mexican avocados—could face permanent American import taxes.

At the company level, agribusiness giants like seed or equipment makers might see sales dip if farmers’ incomes take a hit. As we have been discovering, In every industry, there are second-order effects after the implementation of tariffs.

Food processors relying on imported ingredients could face cost hikes too. Even bourbon got caught in the EU-U.S. crossfire4—Europe’s tariffs on American whiskey dented distillers’ overseas sales.

So, watch for ripple effects on consumer goods, whether through raw materials or export markets.

Retail and Consumer Goods: The Shelf Shock

Finally, retail and consumer goods—anything stocking store shelves. If it’s imported, it’s at risk.

The last trade war woke retailers up when tariffs on Chinese goods drove up costs for toys, appliances, you name it.

Apparel, footwear, toys, and electronics retailers scrambled—some rushed orders, others haggled with suppliers or passed costs to shoppers.

Take toys: Hasbro and Mattel, long reliant on China, faced tariff threats and pivoted production to places like Vietnam and India.

With U.S.-China tensions still high, consumer goods could land back on tariff lists—though many firms have gotten savvier, like fast-fashion brands shifting to Bangladesh or Vietnam.

When analyzing a retailer or brand, have a sense of how sensitive their margins are to cost hikes—luxury players can absorb more than thin-margin discounters. Also, look at inventory: stockpiling ahead of tariffs, as some did in 2019, can skew short-term numbers but cushion the blow.

Mitigation Strategies: Navigating Tariff Turbulence

So, you’ve spotted the tariff risks in your portfolio—what’s the next step? How do you shield yourself or soften the blow? As always, there are plenty of ways to tackle this and there’s nuance, not all mitigation strategies will work in every portfolio. You can click in table below to have a sense of possible actions.

These are of course, general strategies. The tariff landscape in 2025 demands really thoughtful planning.

By assessing company-specific vulnerabilities, recognizing sectoral hot spots, marrying macro insights with micro diligence, leveraging the latest risk tools, and proactively hedging, investors can turn this daunting risk into a manageable aspect of portfolio strategy.

For companies, in many aspects, and even if the tariffs disappear in the following weeks, the damage is already done. Thinking the unthinkable will have to become a recurrent exercise for Canadian and Mexican firms, even for American companies with spread out production systems.

It's a new economy, a more fragmented economy where safety of supply chains and access to markets should not be taken for granted.

The European Union's Carbon Border Adjustment Mechanism (CBAM) is currently in its transitional phase, which began on October 1, 2023, and will continue until December 31, 2025. During this phase, importers must report the embedded carbon emissions in their imports on a quarterly basis, but financial payments are not yet required.

Trade wars have historically not focused heavily on crude oil, but recent events show that oil is increasingly becoming a target in trade disputes. In February 2025, China imposed a 10% retaliatory tariff on American crude oil imports in response to Trump's tariffs.

The Trump administration's 30% tariff on imported solar panels significantly disrupted the renewable energy sector.

During President Trump's first term, he imposed 25% tariffs on steel and aluminum imports, citing national security concerns. In response, the European Union implemented a 25% retaliatory tariff specifically targeting American whiskeys, including bourbon, This retaliatory tariff had a substantial negative impact on the industry: American whiskey exports to the EU (the largest export market for American whiskeys) plunged by 20%, dropping from $552 million in 2018 to approximately $440 million in 2021