The "Why" Question: Rebuilding Investment Theses from the Ground Up

Uncover true investment value by stripping away assumptions and building your analysis from fundamental truths

I’ve been wanting to write about this theme for a while now. It’s something that I haven’t seen being applied to investment write-ups, at least on Substack: the use of first principles analysis in developing investment theses. I have touched on this tangentially in some articles before, but today I’ll do a deeper dive.

Using first principles, we strip a problem down to its bare essentials, the undeniable truths, and then we piece it back together. Instead of accepting the usual assumptions or industry narrative, we have to peel everything back to the core.

This approach forces us to challenge every piece of market narrative. We start fresh, building our conclusions from the ground up with solid facts.

I enjoy doing this for every investment thesis or company I research: identifying the basic facts that are undeniably true about them. I’m sure you’re familiar with the concept and practice of using first principles, but allow me to suggest that applying them consistently from the moment you begin thinking about an investment can make a world of difference.

Understanding First-Principles Thinking in Investing

At its core, it’s about building your reasoning from the ground floor. You ask yourself: 'What do I know for sure about this business, this market, this product?' It’s about breaking the whole thing into its simplest pieces and studying each one with fresh eyes, free from the baggage of 'that’s how it’s always been done.'

Business history if full of such examples.

In the 1970s, airlines were a mess—inflated costs, empty seats, and a “luxury travel” obsession. Southwest’s Herb Kelleher didn’t like it. He asked: What’s an airline’s job? Move people from A to B, fast and cheap. Not fancy meals. Not unnecessary luxury. He tore it down: one plane type (Boeing 7371) to cut maintenance, quick 20-minute turnarounds, no assigned seats, point-to-point routes over hubs. Southwest focused on unit economics (cost per seat mile), and turned profitable while giants like Pan Am bled out. By 2000, it was a top U.S. carrier.

Kelleher rebuilt the model from the fundamental truth—people want affordable, reliable travel.

First-principles analysis dives straight into the nuts and bolts: the specific mechanics and economics that actually make the thing work. Strip it down to the essentials and root your thinking in hard facts.

So, how do we actually insert first-principles thinking into our everyday research? Let’s break it down.

Applying First-Principles to Investment Analysis

Step One: Deconstruct the Business Model

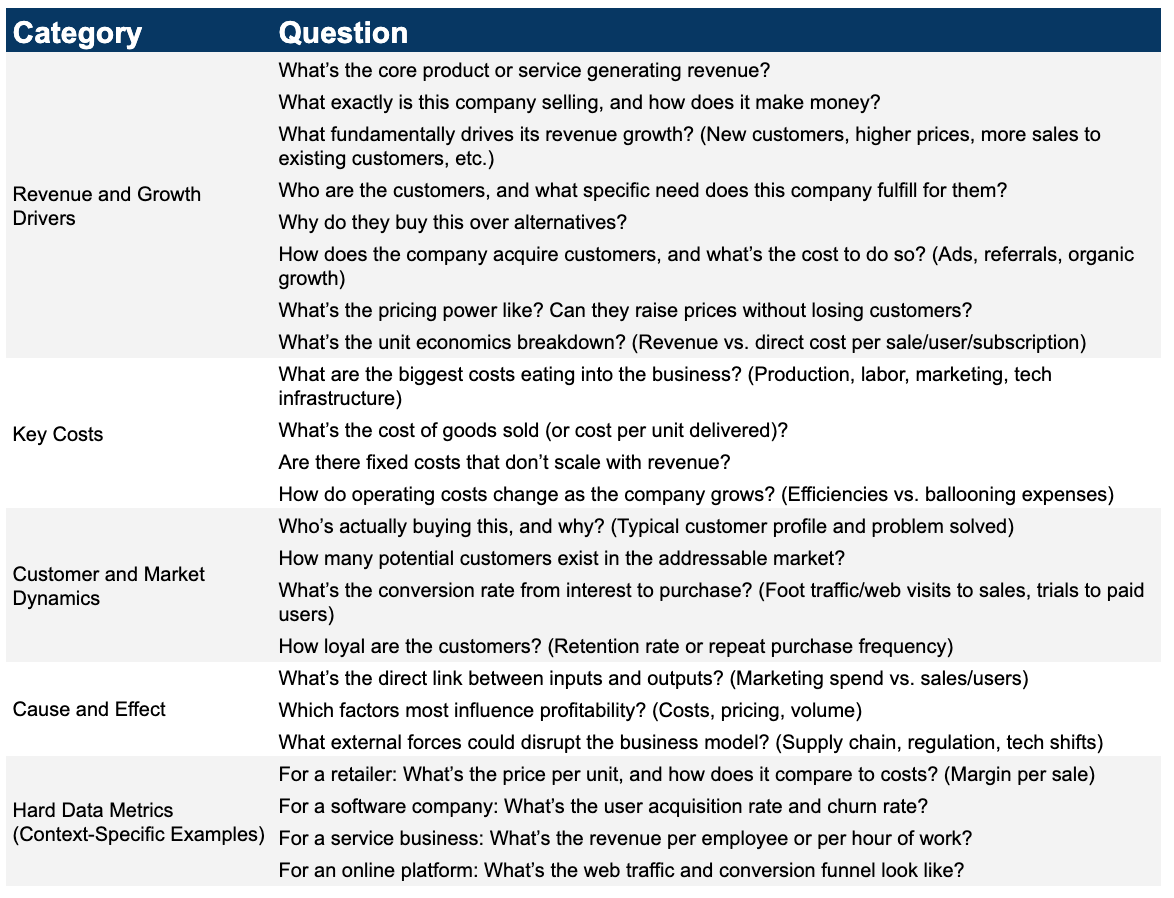

First, take the company apart like it’s a machine. What’s really powering its revenue and growth? What are the big costs? Who’s buying, and what need are they filling? Pinpoint the bedrock factors that drive its value.

For example, if you’re looking at a software company that has been growing 30% annually, don’t just agree and think, 'Well, that’s what software firms usually do.' What else can you find? Dig deeper—check the user acquisition rates, pricing power, unit economics, and competitive edge. Stick to the hard data.

It’s better to think like an engineer taking apart an engine for this phase of the process—you’re tracing cause and effect, not just skimming the superficial performance numbers. Focus on the real drivers—revenue growth, profit margins, competitive advantages—that actually shape a company’s worth.

To help with this step, I created the table below with some questions that may help to jump-start the first principles analysis:

https://docs.google.com/spreadsheets/d/1eFgE4N-hz2iNSH09xCyj8JXa2neMYISFmximSpti9ss/edit?usp=sharing

Step Two: Re-examine Assumptions on Value and Growth

Next, put every assumption under the microscope—yours and the market’s (that’s why I sometimes like to do the reverse DCF model, just to see which assumptions are implied in the stock price).

So, what’s baked into the current valuation? Are we all assuming this company can keep growing at 50% a year? If so, is that rooted in something solid—like a massive untapped market or proven demand—or is it just riding the wave of recent trends? We, as humans, tend to fill in the gaps pretty quickly when we see an up-and-to-the-right trend.

Question the usual suspects: margin growth, customer uptake, scalability—anything that’s often taken as a given.

More often than not, this can shake out some rosy projections that don’t hold up. Ground your take in first-principles realities—like how customer acquisition costs can’t drop below a certain point, or how store sales per square foot hit a ceiling without a new twist.

You might spot cracks in the consensus view that others miss. The point? Tie your valuation and growth bets to what’s economically and physically possible, not some feel-good story.

Again, you can use questions below to bullet proof your analysis:

https://docs.google.com/spreadsheets/d/1eFgE4N-hz2iNSH09xCyj8JXa2neMYISFmximSpti9ss/edit?usp=sharing

Step Three: Compare With Market

Finally, go after the market’s blind spots. Take the thesis you’ve rebuilt from scratch—based on core drivers and realistic assumptions—and stack it against the current narrative.

Where’s the disconnect? Maybe everyone’s saying, 'Industry Y can’t turn a profit,' but your bottom-up work shows a path nobody’s noticed—or maybe the opposite.

Ask yourself: 'What’s the crowd believing about this company or sector, and does that actually line up with first-principles facts?'

By questioning consensus and rebuilding from the ground up, you’re primed to catch what slips through the cracks. Simply put, look where the crowd’s assuming something that isn’t a first-principles truth—that could be where you find the alpha.

That independent view is a game-changer. It lets you bet big on ideas you’ve cracked at a fundamental level and steer clear of overcrowded trades resting on flimsy guesses. I wrote more about this here:

https://www.polymathinvestor.com/p/the-twin-engines-of-increased-conviction

The Superpower of Starting from Scratch

By constantly asking “why?” and drilling down to bedrock truths, you avoid the shallow narratives that populate so many write ups and instead build an investment thesis on solid ground.

I believe this approach is powerful because it marries creativity with discipline: you’re not just thinking differently for the sake of it, you’re thinking from the foundation up.

It’s more work upfront, no question. Yet that effort can uncover insights that others miss—insights that could translate into serious outperformance.

Are you ready to challenge the consensus and rebuild your next investment thesis from the ground up?

Southwest adopted an exclusive Boeing 737 fleet strategy (with only minor exceptions later in its history), which dramatically reduced maintenance costs, simplified crew training, and streamlined operations. This uniformity allowed for greater efficiency in maintenance procedures and operational planning.

Thank you so much for your generous sharing & education!

Very good and useful! Thank you very much.